February 13, 2024

When you consider your nonprofit’s finances, the first thing that comes to mind is likely your fundraising revenue. After all, running campaigns and bringing in donations year-round takes up a lot of your team’s time and energy, and individual contributions probably make up the bulk of the funding your nonprofit uses to fulfill its mission.

However, effective nonprofit financial management extends beyond just raising as much money as possible. To ensure the best possible financial situation for your organization, you’ll also need to properly allocate, track, and report your revenue.

In this guide, we’ll help you get started by breaking down four key areas of nonprofit finance, including:

- Creating an Annual Operating Budget

- Cultivating Reliable Revenue Sources

- Developing Fiscal Policies

- Compiling Financial Statements

With these strategies in your toolkit, you’ll be able to lay a solid foundation for effective financial management at your organization. Let’s dive in with an overview of the most important financial planning document at your disposal: your operating budget.

1. Creating an Annual Operating Budget

Your nonprofit’s annual operating budget is the master financial plan that guides all of your spending and fundraising throughout the year. It breaks down the expenses you plan to incur as well as the various types of revenue you’ll bring in to cover those costs.

To make your annual operating budget as useful as possible, Jitasa’s nonprofit budgeting guide offers the following tips:

- Clearly define all activities. Your nonprofit’s budget should line up with the initiatives laid out in your current strategic plan. For instance, if one goal of your strategic plan is to increase your organization’s online presence, you should have a section devoted to digital marketing in your expenses section that lays out how much you plan to spend on activities like website development, online advertising, and graphic design.

- Budget for specific time periods. Your operating budget will typically cover one fiscal year, but you’ll need to consider what times of year your organization brings in the most and least revenue. Nonprofit donations often peak at the end of the year and die down during the summer, so you might make a note in your budget to save some money from your year-end giving campaign to help cover the following summer’s expenses.

- Set realistic goals. Review your previous year’s fundraising totals and current financial situation to determine if the numbers you’ve predicted for each revenue source are reasonable. For example, if your organization raised $80,000 in major gifts last year and $75,000 the year before, your prediction for this year might be $85,000 as long as your nonprofit is still on a growth trajectory.

Although you’ll create a new operating budget once a year, budgeting shouldn’t be a one-and-done activity. At least once a month, check in with your budget to help keep your nonprofit’s spending and fundraising on track.

2. Cultivating Reliable Revenue Sources

A key reason that nonprofit finance is complex is that nonprofits typically bring in revenue from a variety of sources. However, effective revenue generation requires fundraising sustainably for year-round financial success.

Here are some common nonprofit revenue sources you can use to develop a sustainable funding model:

- Individual donations. These typically make up the bulk of a nonprofit’s funding and include all sizes and types of gifts. While acquiring new donors is sometimes helpful for growth, focusing on retaining existing donors will provide more stability from this revenue source. Follow up quickly and consistently with each donor, and make it easy for them to give on a recurring basis.

- Corporate philanthropy. This includes all of the ways businesses support nonprofits financially, whether that’s through sponsoring an event or matching their employees’ donations. Work on building relationships with your corporate supporters to form long-term, mutually beneficial partnerships with them.

- Grants. Although grants can be competitive, they often provide essential funding for your nonprofit’s most important projects and initiatives. If you can secure a grant and demonstrate to the grantmaker that you’ve properly managed the funding they awarded you, they’ll be more likely to support your organization again.

- Investments. If you have revenue left over after covering your expenses for the year, investing is a great way to grow your organization’s long-term savings. Nonprofits can open brokerage accounts just like individuals can, plus they can invest in stocks, bonds, and even cryptocurrency.

Besides helping with budgeting, having several sustainable revenue streams will increase your organization’s financial security. If financial difficulties arise or unforeseen expenses come up, you may still be able to cover your nonprofit’s costs and adjust your budget more easily.

3. Developing Fiscal Policies

Fiscal policies set the standard for how your organization manages its finances day to day. Plus, they help ensure compliance with nonprofit legal requirements and allow you to stay accountable to the supporters and stakeholders who make your mission possible.

The most important fiscal policies to implement at your organization include the:

- Gift acceptance policy. This guideline details the types of contributions (both financial and in-kind) your organization can and can’t accept, as well as the circumstances under which you can receive each type of donation. This way, if a well-meaning supporter gives a gift you can’t accept, you have official documentation to back up your rejection and reduce the risk of coming off as ungrateful.

- Conflict of interest policy. This policy prevents your nonprofit’s board members and leadership from making decisions that are influenced by outside financial interests rather than their duty to your organization. It outlines what situations could be considered conflicts of interest and what steps to take if a conflict arises.

- Expense reimbursement policy. When staff members or volunteers spend their own money on behalf of your organization’s work, you can reference this policy to determine whether and how you’ll go about repaying them. It helps prevent fraud by confirming that all reimbursed funds were actually used on your nonprofit’s behalf.

- Staff compensation policy. This guideline details how each of your nonprofit’s employees will be compensated for their work to ensure everyone is paid fairly and not excessively. When developing this policy, Astron Solutions recommends taking a total rewards approach, meaning you should include information about staff members’ direct compensation like salaries and indirect compensation like health insurance and paid time off.

Create a fiscal policies and procedures document to ensure all of this financial management information is recorded in one place for your staff and board to easily reference.

4. Compiling Financial Statements

Financial statements are accounting documents that organize and summarize financial data in specific ways. In addition to being necessary for compliance, these reports can provide important insights into your organization’s financial situation that you can use to make informed decisions.

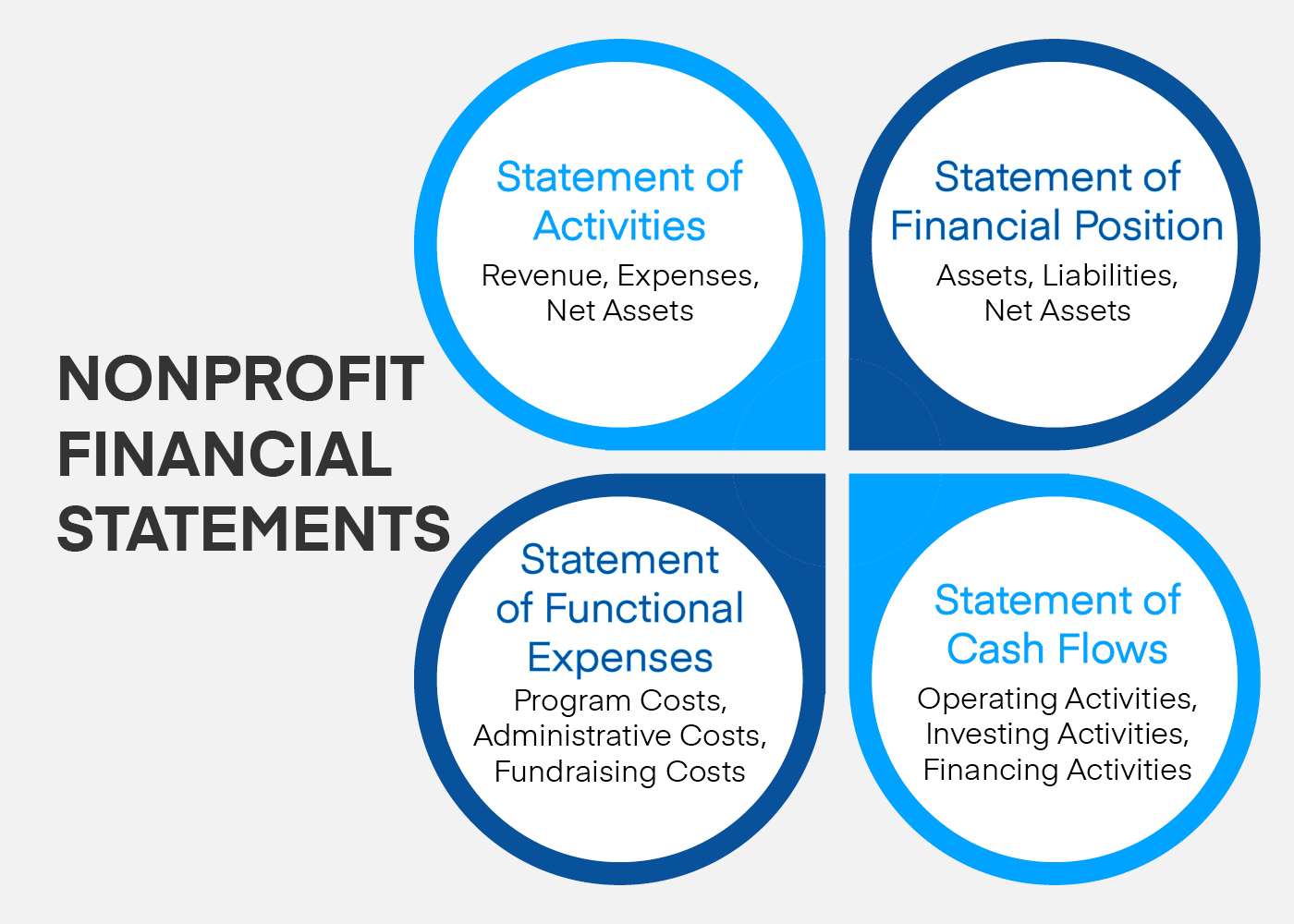

The four core nonprofit financial statements are the:

- Statement of activities. The nonprofit parallel to the for-profit income statement, this report summarizes your annual revenue, expenses, and net assets and is helpful in the budgeting process.

- Statement of financial position. Also known as a balance sheet, this statement provides a snapshot of your organization’s financial health by breaking down your assets, liabilities, and net assets.

- Statement of cash flows. This report shows how cash moves in and out of your nonprofit each month through operating, investing, and financing activities to help keep your spending and fundraising on track.

- Statement of functional expenses. This statement, which is unique to nonprofits, demonstrates how your funding furthers your mission by categorizing expenditures based on whether they’re used for program, administrative, or fundraising activities.

Besides serving as a reference for your organization’s financial planning and analysis, these statements help in filling out your nonprofit’s annual tax return. Additionally, many nonprofits include information from their financial statements in their annual reports to increase transparency with supporters.

Your nonprofit’s financial management strategy works side by side with fundraising to accomplish your goals and serve your community effectively. These four areas of consideration will get you well on your way to understanding nonprofit finances and applying them as you further your mission. However, don’t hesitate to reach out to financial experts if you need help or have any questions along the way.

-2.png)